The Fed reached its inflation target years ago. It just never noticed. Part 2.

The Fed reached its inflation target years ago. It just never noticed. Part 2.

Part 2. What has happened in recent years, what’s going on in 2021

First published: November 2021. Last update: Feb 2022

This study is a compilation of my articles published on online financial journals Portfolio and ConcordeBlog during 2020-2021.

-------

As a result of misinterpretations of inflation and deflation, central banks rely on false signals and make wrong decisions. In recent years, they failed to recognize inflation and remained way too expansionary way too long. Earlier, they saw inflation where there was not, and exacerbated recessions by unjustified tightening. The correct interpretation of price changes and the localization of surplus money would lead us to better monetary policy decisions.

-------

Part 1. Neither inflation nor deflation is what it seems

-------

What has happened in recent years, what’s going on in 2021

2000-2020

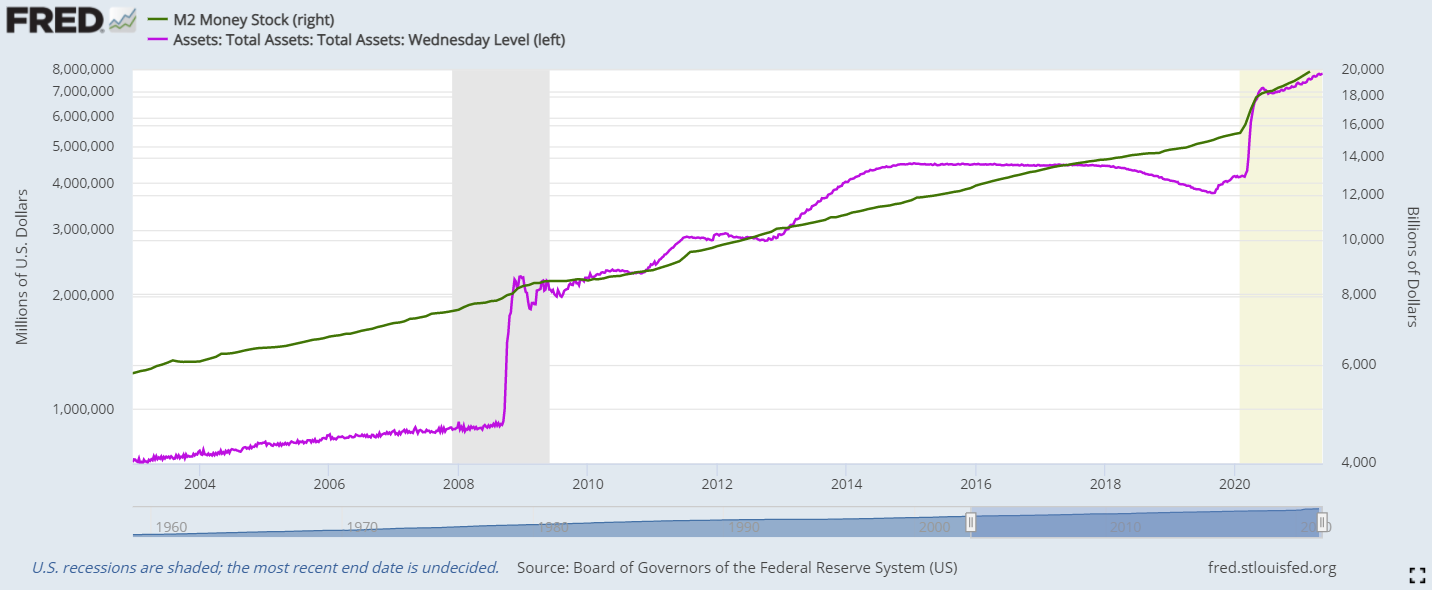

In 2008-2009, the Fed did not print money

The multiplication of the Fed's balance sheet during 2008-2009 (and later again in 2013-2014) did not lead to a multiplication of the total amount of dollars in circulation, what’s more, money supply did not increase by as much as the central bank balance sheet grew at all. The reason behind is that by increasing its balance sheet the Fed primarily supplied the increased money demand of a banking system that was in trouble, as well as the elevated demand for safe assets by economic agents.

The multiplication of the Fed's balance sheet was not money printing, much of it was not even money creation, because most funds provided to banks did not leave the banking system, did not enter the economy. Banks did not increase lending due to a relatively weak economy and to heightened wariness by banks.

In 2008-2009, and in 2013-14 the intervention of the Fed almost did not create money at all. In 2020, it did. Source: Federal Reserve Bank of St. Louis

Commercial banks, on the other hand, did print

Banks became cautious after the 2008 crisis for a reason: earlier, before the crisis, they were lending money on a giant scale even by global standards and often, without doubt, irresponsibly. They were printing money.

The Fed’s balance sheet expansion during the 2008-2009 crisis was not money printing, not even money creation, rather just keeping the money printed by commercial banks in preceding years in circulation, in order to keep the banking system alive.

The depreciation of the dollar in the 2000s is well represented by the march of gold. Source: Scott Grannis

Savers are rolling in money

At the same time, there’s an abundance of money in the markets also from other sources: the long-term savings of the developed world.

The developed world has been accumulating for decades for retirement, emergencies, travel, housing, and keeps its savings in bank deposits, corporate and government bonds, equities. The distribution of savings is extremely unequal, but the total amount is huge, still growing, and is hopelessly hungry for returns in all areas of the investment world.

The chart only shows bank deposits and only for the US. The range of financial savings is much wider. Source: Federal Reserve Bank of St. Louis

2020

The Fed remedied the scarcity of money by creating money

In March 2020, life came to a halt, business and financial processes froze, the circulation of money slowed down massively, those who had liquid assets, turned them into cash, who had cash, stuck to it. Due to the slowdown, the economy's money demand increased significantly resulting in a brutal scarcity of money. The Fed, as the commander of the dollar system, made up for this severe scarcity of money with fresh money poured onto the markets.

Compensating for the relative scarcity of money is an adequate decision, justifiable money creation that does not result in excess money, it is not money printing, it does not depreciate the currency, it is not an inflation of the currency.

In modern banking systems, the relative scarcity of money is normally compensated for by commercial banks via intensified lending. In March 2020, however, commercial banks were in scarcity of money themselves, the central bank had to intervene and create additional money. The Fed’s quick and appropriate action limited the economic damage caused by the pandemic.

In 2020, though, the Fed did not just make up for the relative scarcity of money.

The Fed also got into politics

In 2020, the Fed also made another important decision: though indirectly, it started financing the government’s disaster relief programs. This was no longer a monetary policy decision, it was a social and economic policy resolution that should be judged as such.

The Fed financed government aid programs by printing money, by inflating the dollar. Essentially, the Fed spread the cost of the aids among all dollar holders since this was the fastest possible financing solution at such a scale. Slower solutions (taxes) are also in the making by the government by now.

2021

Goods getting pricier and inflation at the same time

Year 2021 is special because we see on the one hand goods becoming pricier and on the other hand inflation at the same time, and it’s terribly hard to tell the difference.

The relaunch of the economy caused a sudden surge in demand while the supply of goods is expanding slowly. The result: shortages and rising prices in the chip sector, in used cars, in construction raw materials, and in all areas of the hospitality industry. This is, in the first place, 'goods getting pricier’, not inflation, because the rise in prices is primarily not a result of the depreciation of money.

What is happening is that wherever industries are still rolling only at half speed, the available products have become more valuable for customers and therefore the price of these more valuable products has gone up. The Fed has nothing to do with it. It’s not hiking rates on New Year's Eve either, despite the price of a wide range of products and services steeply increasing due to a jump in demand.

At the same time, it is undeniable that in 2020 and 2021 the Fed poured a lot of money into money markets and explicitly printed money to finance the government, in addition to being way too loose for years due to a misunderstanding of deflation and not recognizing inflation. As a result, we can firmly claim that there is excess money in the economy and that it inevitably leads to inflation and a strengthening of future inflation expectations.

The two key questions are how much excess money there is and where it flows, that is, where it causes inflation.

And of course there is a third question: what should be done about it.

Inflation only became easily detectable in asset prices

Although the economic-financial system is full of excess money, strangely, surplus money has only raised the price of investment assets dramatically.

Asset prices rose because:

an overwhelming part of excess money is in the hands of the wealthy, who mainly spend it on investments not consumption (and when they buy luxury goods, those Ferraris and Patek Philippes do not balloon the CPI),

also because modern, flexible production processes turn increased consumer demand into profit without an increase in product prices, and, of course, profits will also seek investment opportunities in the investment assets market,

as well as because excess money could be eliminated from the economy via loan repayments, but it’s not eliminated because almost all excess money is in the hands of those who do not have loans to be repaid, or, if they have, at the current, extremely low rates, repayment is not an attractive idea (actually today, getting indebted is what seems to be an attractive idea).

We see an interesting phenomenon in the real estate market, which is both an investment assets market and a consumer goods market, and where inflation has resulted in record high prices but rents have not risen proportionately due to low interest rates. Inflated asset prices did not inflate the CPI.

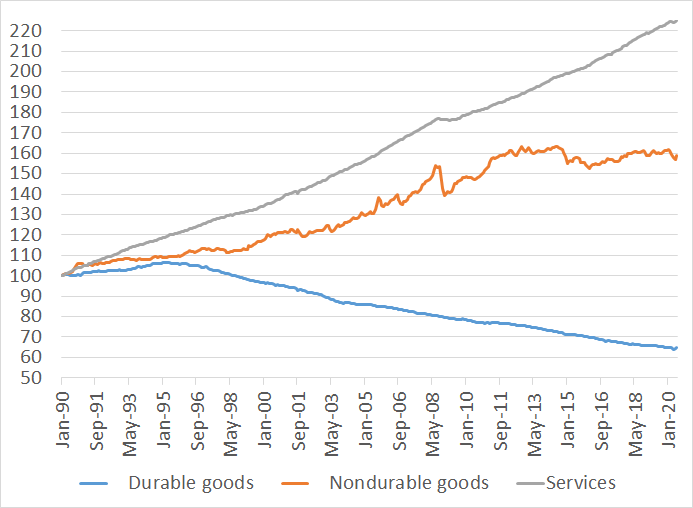

Actually, there was inflation in consumer goods markets too

Although consumer price indices remained at moderate levels throughout the last 20 years, low index figures were the products of two very different mechanisms:

decreasing prices due to innovation, globalization and tax cuts that was considered deflation incorrectly, and

actual and significant inflation in several other consumer goods markets (see, for example, education, health, services).

Durable consumer goods prices: -35% in 25 years. Source: Bureau of Economic Analysis

Many say that technology is deflationary. That’s a misunderstanding of money and deflation. Decreasing prices of durable and technology goods were not a monetary phenomenon, while the inflating prices of services they were. The arising blend completely mislead central banks.

Due to investment asset inflation not being measured by consumer price indices, and due to consumer goods inflation that was concealed in consumer price indices by non-monetary factors, the real rate of inflation for sure has been significantly higher than the CPI for a long time.

The Fed reached its inflation target years ago. It just never noticed.

-------

End of Part 2. To be continued.